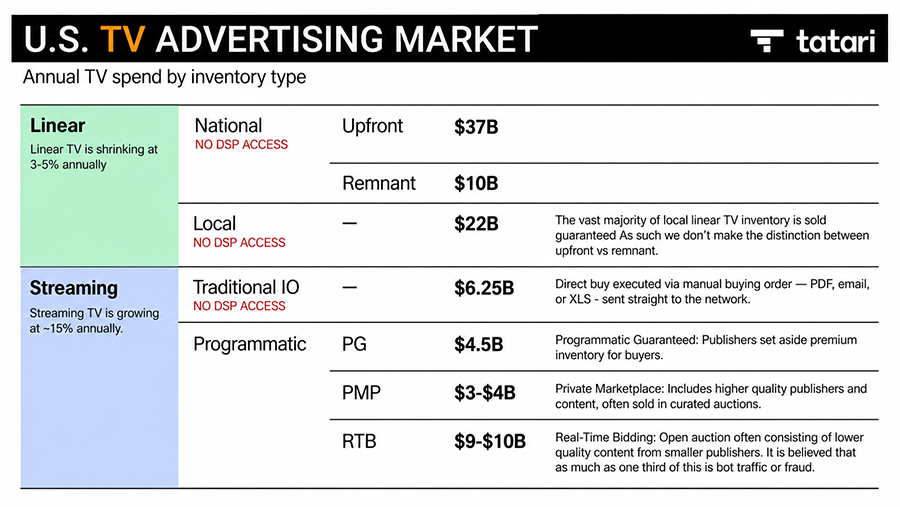

| National linear: the upfront market

National linear alone accounts for roughly $47 billion, split between upfront commitments and scatter inventory. Upfront deals represent annual commitments negotiated directly between agencies and networks at pricing not available anywhere else. This market runs on relationships built over decades.

Local linear: the fragmented billions

Local linear is expected to hit $21 billion, driven in part by political ad spend. It is highly fragmented with regional networks, cable operators and broadcast affiliates selling inventory manually, largely outside any automated system.

For national brands with regional presence, this market is difficult but not impossible to access. For local advertisers, it remains one of the most important channels available.

Streaming: traditional insertion orders

Streaming is growing at roughly 15% annually and now accounts for 47% of all TV viewing in the US, according to Nielsen’s latest Gauge report. This is where programmatic makes sense and where most of the industry conversation has concentrated.

But streaming inventory is not a single market. The stack runs from traditional direct IOs at the top, then programmatic guaranteed and private marketplace deals, down to open RTB at the bottom. Premium direct inventory, the kind bought through upfront-style deals with major publishers, doesn’t enter programmatic pipes. And roughly 20% to 25% of all ad-supported streaming inventory can only be purchased via linear.

Open auction: the slice of streaming that DSPs actually touch

The programmatic tier of the streaming market comprises programmatic guaranteed (PG), private marketplace (PMP) and open RTB, representing roughly $17 to $18 billion. This is the pocket where DSPs operate.

Limiting your TV strategy to this tier doesn’t mean you’re buying TV. It means you’re buying a sliver of it, shrinking the opportunity from a $90 billion market to a $15 billion one. The cleanest inventory in that sliver isn’t guaranteed. By some estimates, as much as one-third of open RTB CTV inventory involves bot traffic or invalid impressions.

The hidden cost of what programmatic does reach

Even within the programmatic tier, the economics are not what they appear.

The supply chain between an advertiser and a publisher can include a DSP, an SSP, a reseller and multiple auction intermediaries. Each takes a cut. The aggregate cost, what the industry calls the ad tech tax, can consume a significant share of every media dollar before it reaches actual inventory. Tatari publishes real campaign data at adtechtax.com, comparing direct buys against the same inventory purchased through programmatic pipes. The difference is not marginal.

There is also a structural argument that the complexity of that chain was never justified for TV in the first place. On the open web, aggregation technology solves a real problem, navigating hundreds of thousands of fragmented publisher sites.

TV has the opposite problem. Internal Tatari platform data from hundreds of millions of dollars in measured spend shows that roughly 90% of CTV impressions come from just 10 publishers. The supply is sufficiently concentrated that the intermediary layer isn’t solving the complexity. It is creating cost.

This isn’t accidental. DSP algorithms optimize for platform outcomes such as fill rates, take rates and margin. The infrastructure and the advertiser are not always working toward the same goal.

Programmatic is an access point, not a strategy

A DSP is one way to buy TV. It is not TV itself.

The most effective TV campaigns are built across the full ecosystem. The marketers executing them buy in the upfronts when securing high-performing inventory makes sense; they understand the right mix of local when it matters; they run campaigns across linear and streaming together; and they use the power of programmatic for hyper-targeted audiences.

Getting there requires infrastructure built for the full TV ecosystem. Nearly 90% of advertiser spend on Tatari’s platform is bought directly from publishers through Upstream, connecting advertisers to publishers at the ad server level—no DSP, no SSP, no unnecessary intermediaries. The remaining 10% is programmatic, where it genuinely works.

The brands winning on TV aren’t anti-DSP. They’re anti-ceiling. Programmatic is part of how they buy, not the limit of what they can buy. |